Financial Independence with the SMART Goals Method

In brief

- ▸Financial independence: having enough wealth to cover your lifestyle without depending on a salary.

- ▸SMART method: every financial goal must be Specific, Measurable, Achievable, Relevant and Time-bound.

- ▸Your number: multiply expected annual expenses by 25 (4% rule) to calculate the target portfolio size.

- ▸Monitoring: a portfolio tracker like DonkyCapital shows your exact distance from your goal in real time.

- ▸Adaptation: SMART goals are reviewed annually based on changes in context and markets.

"I want to become financially independent." It is one of the most common goals among people who start investing seriously — but in most cases it remains a vague wish, lacking the structure needed to become a concrete plan. The difference between a dream and a goal is precision: knowing exactly where you want to go, by when, and how to measure progress along the way.

The SMART goals method — born in management but perfectly applicable to personal financial planning — provides exactly this structure. This guide walks through how to apply it step by step to your investment portfolio, which tools to use to monitor progress, and how to connect long-term goals to daily investment decisions.

What Does Financial Independence Really Mean?

Financial independence (FI) does not necessarily mean stopping work or living off passive income on an island. It means having enough wealth to generate passive income that covers your lifestyle — without depending on a salary. FI has different levels, and understanding which level you want to reach is the first SMART step:

Coast FIRE

You already have enough: compound interest will do the rest until retirement without further saving.

Lean FIRE

Passive income covers essential expenses with a frugal lifestyle.

Fat FIRE

Passive income covers your current lifestyle in full, without compromise.

Defining which level you want to reach is not a detail: it radically changes the target wealth, the time horizon and the required savings rate. It is the starting point of any well-built SMART goal.

How Do You Apply SMART Goals to a Portfolio?

SMART stands for Specific, Measurable, Achievable, Relevant, Time-bound. A vague goal like "I want to be rich" has no traction: you do not know where to start, you cannot measure progress, you do not know when you have arrived. Applying the SMART filter, the same desire becomes a plan:

Specific

"I want to build a €750,000 portfolio to cover €30,000/year in expenses without earned income."

Measurable

"The portfolio value is trackable daily in real time on DonkyCapital."

Achievable

"Investing €1,500/month at 6% p.a., compound interest confirms feasibility in 18 years."

Relevant

"Reaching financial freedom before age 55 is aligned with my values and life priorities."

Time-bound

"I want to reach this goal by age 55 (18 years from today)."

The specificity of the goal turns planning from abstract to concrete. Only with a precise goal can you calculate the current gap, simulate different scenarios and measure progress with real data.

How Do You Calculate Your Financial Independence Number?

The starting point is the "4% rule" from the Trinity Study: in a well-diversified stock/bond portfolio, you can withdraw 4% of the initial value each year (inflation-adjusted) with a high probability of not exhausting capital over 30 years. This means:

Base formula

Target wealth = Annual expenses × 25

Example: €30,000/year × 25 = €750,000 — Fat FIRE with €50,000/year × 25 = €1,250,000

This number is your main SMART goal — the one to enter in your portfolio tracker and compare with your current wealth. The difference is your "FI gap": the distance to close with savings and investment returns. Keep in mind that the 4% rule was developed in a specific market and tax context (USA). In countries with different capital gains and dividend tax rates, a more conservative estimate (3–3.5%) is often more prudent. Expected inflation in your country of residence also matters for long-term planning.

What Tools Help You Monitor Progress?

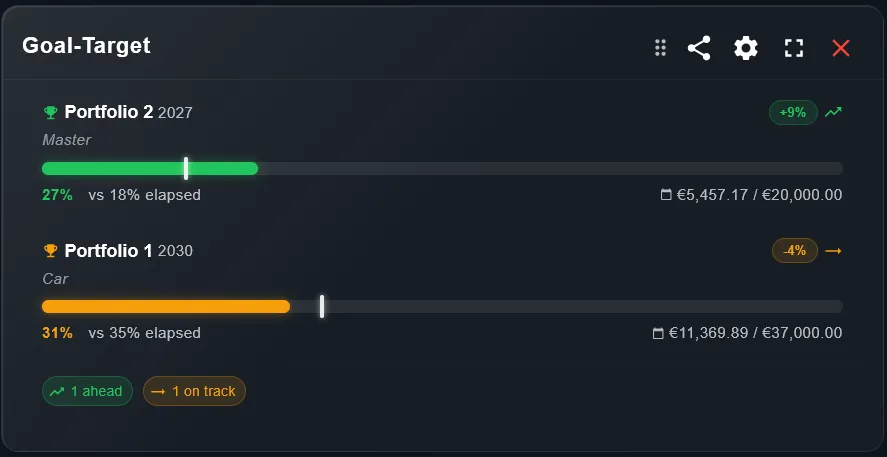

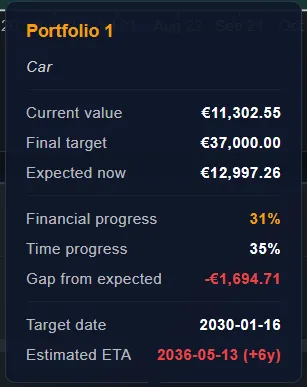

A SMART goal without systematic monitoring is just an aspiration. To turn it into a plan that works in practice, you need to see at any moment: total portfolio value, asset class composition, historical and projected return, and distance from the final goal. DonkyCapital automatically aggregates all your accounts across brokers (Degiro, Scalable Capital, Trade Republic and more) in a single dashboard, calculating actual performance (TWR and IRR) and comparing against your benchmark.

DonkyCapital goal widget showing progress toward the target portfolio value

Detail view with milestones, projected achievement date and remaining gap

Linking your portfolio tracker to your SMART goal turns an abstract figure into a concrete progress bar that updates daily. This kind of continuous feedback is proven to increase savings discipline and the probability of reaching the goal. Seeing the number grow — even slowly — reduces the risk of abandoning the plan during difficult phases.

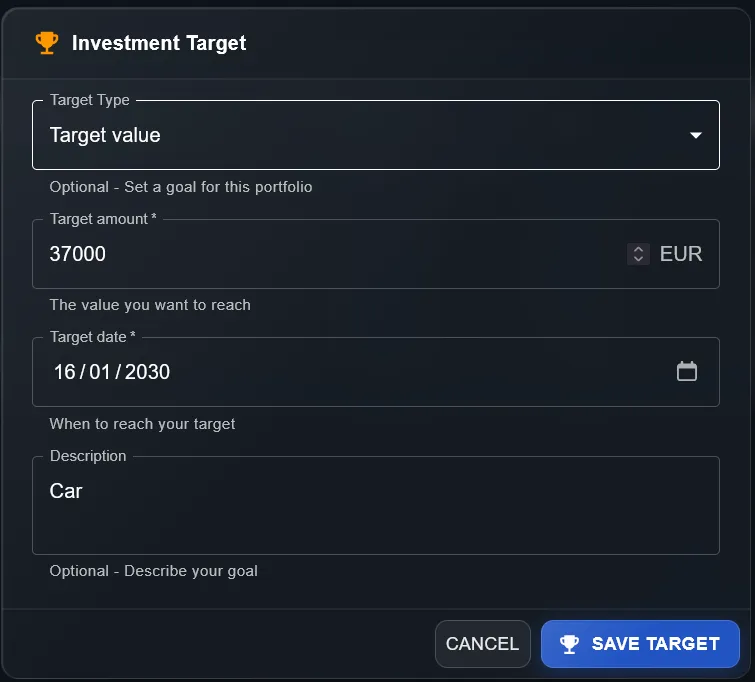

Setting the target value for a financial goal

Setting the target annual return rate for the projection

The SWR (Safe Withdrawal Rate) simulator in DonkyCapital lets you calculate how many years of sustainability your portfolio has at different withdrawal rates — an essential tool for anyone approaching the decumulation phase who wants to verify the feasibility of their plan with historical and stochastic scenarios.

How Do You Adapt SMART Goals Over Time?

SMART goals are not set in stone. Life changes, markets change, and the plan must adapt. A portfolio that suffered a 30% crash in one year does not require panic — it requires a plan review. A year in which you saved twice the expected amount is the opportunity to move the finish line forward. Annual goal review is an integral part of the method: not an admission of failure, but an act of financial maturity.

Annual review checklist

- ✓Recalculate expected annual expenses in retirement (have they changed?)

- ✓Update your FI number with revised expenses × 25

- ✓Check the current gap: current portfolio vs. target portfolio

- ✓Calculate whether the savings rate is still aligned with the timeframe

- ✓Compare actual return (TWR) with the return expected in the plan

- ✓Review allocation and check whether rebalancing is needed

- ✓Update the projected date in your portfolio tracker

FAQ on Financial Independence and SMART Goals

What is the difference between FIRE and financial independence?

FIRE (Financial Independence, Retire Early) is a specific version of FI targeting early retirement, often before 50. Financial independence is broader: you can be FI and continue working by choice, not necessity.

How long does it typically take to reach financial independence?

It depends on savings rate. Saving 10% typically takes 40+ years. Saving 30% can achieve FI in 25-28 years. Saving 50%+ may take 15-17 years. Investment returns and expected expenses are the other key variables.

Is the 4% rule applicable regardless of where you live?

The 4% rule comes from the Trinity Study (USA) and needs to be adapted to the local context. Capital gains and dividend tax rates, expected inflation and the public pension system vary significantly by country. A more conservative rate of 3–3.5% is often more prudent outside the USA. Always consider the net after-tax return.

How do I use DonkyCapital to track progress toward financial independence?

You can set your FI number as a portfolio goal, aggregate all your brokers and accounts, and see in one dashboard how far you are from the target. The SWR simulator lets you calculate how many years of sustainability your portfolio has at different withdrawal rates.

Do I need a financial advisor to set SMART goals?

Not necessarily. The SMART method is a self-planning tool you can apply independently. An advisor is useful for specific aspects like tax planning or succession. For monitoring investments, tools like DonkyCapital cover most operational needs.

What happens to SMART goals if the market drops 40% during my accumulation phase?

A 40% drop temporarily moves the finish line — but it is also the opportunity to buy at much lower prices, accelerating wealth building through dollar-cost averaging. The annual SMART review covers exactly this scenario.

Is it better to have one big FI goal or several sub-goals?

Both approaches work. Having intermediate sub-goals (e.g. "€100,000 in 3 years", then "€300,000 in 7 years") helps maintain motivation and verify you are on track in the short-medium term. DonkyCapital lets you set intermediate milestones within the main goal.

Track Your Path to Financial Independence

Aggregate all your brokers and accounts on DonkyCapital, set your goal and follow your progress toward financial freedom with precise data.

Start for free