The Market Timing Trap: why Rebalancing is your best ally

In brief

- ▸Market timing: trying to buy at lows and sell at highs is proven to fail over the long term.

- ▸Cognitive biases: fear, greed and FOMO systematically distort investment decisions.

- ▸Real cost: missing the 10 best market days in 20 years can cut your final portfolio return in half.

- ▸Rebalancing: a mechanical reallocation rule removes emotion and turns volatility to your advantage.

- ▸Automatic alerts: DonkyCapital monitors drift from target and notifies you only when it is truly time to act.

Every time markets drop 10%, millions of investors think the same thing: "Maybe I should wait for things to stabilize before buying." And when markets rise: "Maybe it is too late — I will wait for the next dip." This mental loop has a name: market timing. And it is one of the most costly mistakes an investor can make — regardless of experience level.

The good news is that there is a systematic alternative, based on rules rather than emotions: periodic portfolio rebalancing. This guide explores why market timing does not work, which cognitive biases fuel it, how much it actually costs in practice, and how a mechanical rebalancing strategy can turn volatility from enemy to ally.

What Is Market Timing and Why Does It Seem Appealing?

Market timing is the practice of trying to anticipate market movements — buying before rallies and selling before downturns. In theory it sounds reasonable. The problem is that nobody — not even professional managers with teams of analysts — can do it consistently over time. SPIVA research shows over 90% of actively managed funds underperform their benchmark over 15 years. Not because managers are incompetent, but because the market already prices in all available information. Market timing is not a competence problem: it is a structural one.

"Every time you exit the market you must make two correct decisions in a row: when to exit AND when to re-enter. Getting either one wrong wipes out any potential benefit." — a fundamental principle of behavioral finance

In practice, the average investor who tries to time the market does not just fail to beat it: they systematically underperform the passive investor who simply stays invested. This holds for equity markets, bond markets, and even cryptocurrency markets, where volatility amplifies the damage of timing attempts even further.

Which Cognitive Biases Fuel Market Timing?

Our brains are evolutionarily programmed to respond to immediate threats, not to reason about long-term probabilities. This generates a series of systematic biases that lead investors to make poor decisions at the most critical moments:

Loss aversion

A 10% loss feels almost twice as painful as an equivalent gain (Kahneman & Tversky). This drives panic selling to "lock in" the loss.

Confirmation bias

After deciding to exit the market, you seek only news that confirms the decision. Positive news is ignored or dismissed.

FOMO (Fear Of Missing Out)

Drives buying after a strong rally — exactly when prices are already elevated and the risk of correction is high.

Recency bias

Recent trends are projected into the future: after a crash you expect the crash to continue; after a rally you expect the rally to never end.

Anchoring bias

You mentally anchor to the purchase price or the all-time high. You wait to "break even" before selling, even when fundamentals have changed.

Overconfidence

After a few lucky trades, you tend to overestimate your forecasting ability, increasing the frequency and size of speculative moves.

Recognizing these biases is the first step to not falling victim to them. But awareness alone is not enough: in moments of strong emotional stress (sudden crash, bull market euphoria), even the most disciplined investors can give in. The real defense is having a mechanical rule defined in advance — and a tool that reminds you to follow it.

What Does Market Timing Actually Cost in Real Data?

Looking at the numbers is the most effective way to understand the real damage of market timing. JPMorgan publishes in its annual "Guide to the Markets" a particularly illuminating analysis of what happens to investors who miss only the best days of the market — typically due to an emotional exit.

>90%

Active funds underperforming benchmark over 15 years (SPIVA)

−53%

Return lost over 20 years by missing the 10 best days (JPMorgan)

−1.5%/yr

Average behavioral gap vs. fund return for self-directed investors (Morningstar)

The 1.5% annual behavioral gap documented by Morningstar may seem modest, but over a 20-year horizon it translates into a total return difference of over 30%. The best market days often come immediately after the worst crashes — exactly when fear drives investors out of the market. Those who exit in panic miss the sharpest recoveries, which are also the most important for portfolio recovery.

How Does Systematic Rebalancing Replace Market Timing?

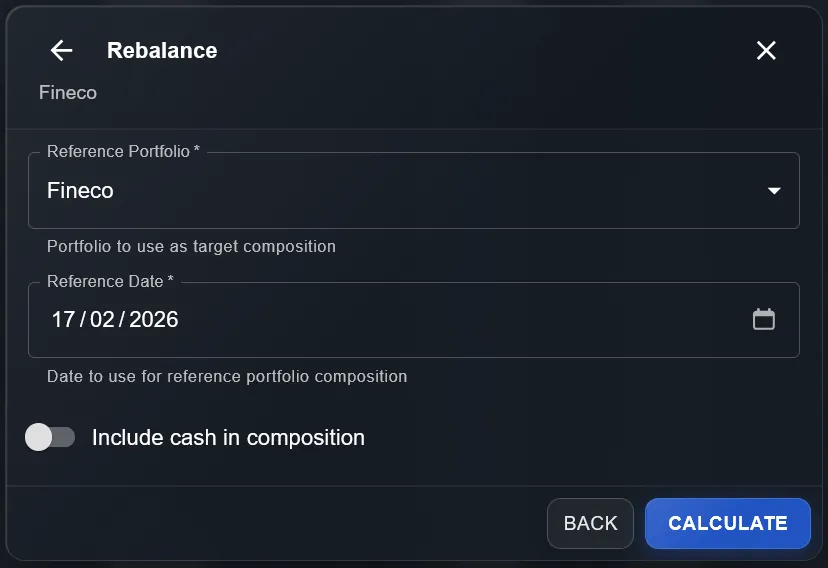

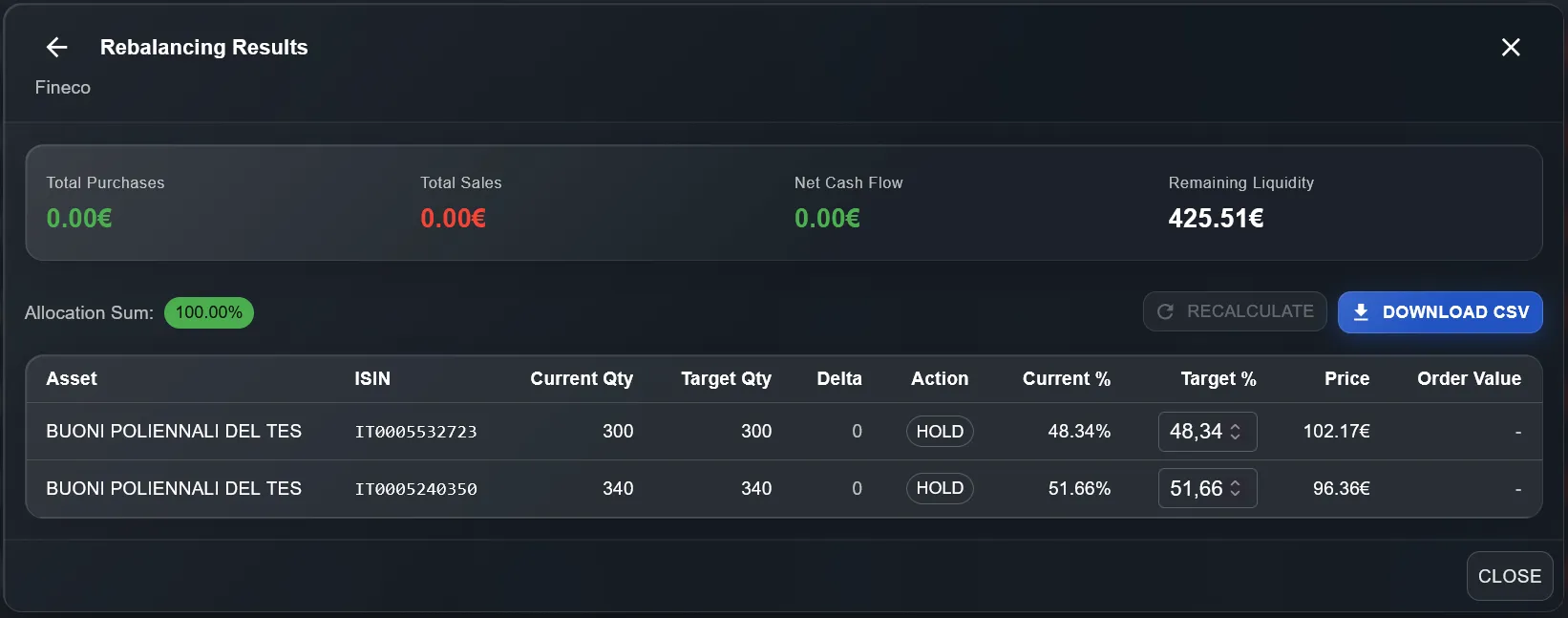

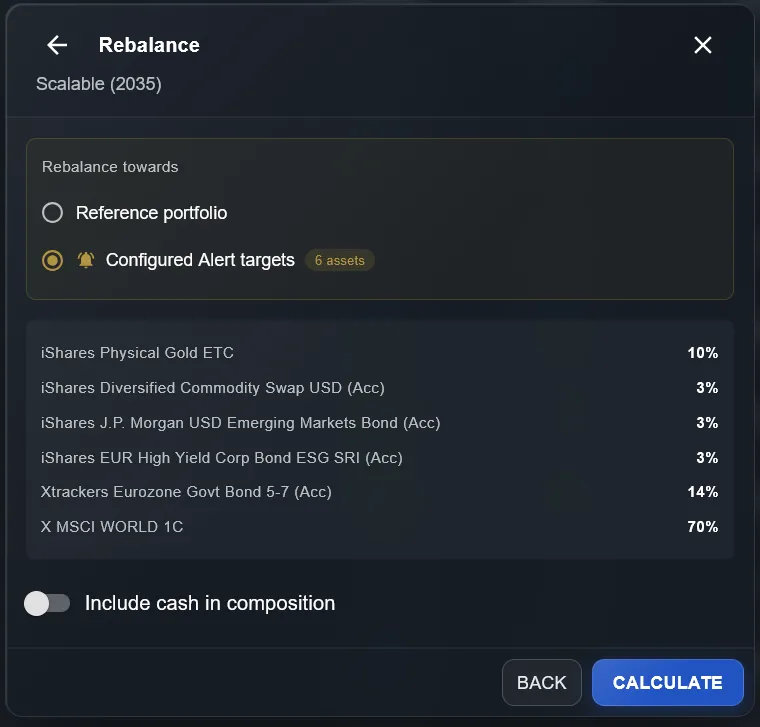

Rebalancing is the emotional opposite of market timing: instead of following emotions, it follows a mechanical rule. You define a target allocation in advance (e.g. 70% equity, 30% bonds) and act only when drift exceeds a preset threshold (e.g. 5%). This means automatically buying what has fallen (buy low) and selling what has risen (sell high) — but systematically, not speculatively. Rebalancing eliminates analysis paralysis: the rule is defined in advance, so no decision needs to be made at the emotionally most difficult moment.

DonkyCapital shows the current allocation drift from target for each asset class

Result after rebalancing: allocation returns to target with the minimum necessary operations

Over the long term, rebalancing can add return through the so-called "rebalancing bonus" — the systematic capture of volatility. Selling what has risen above target and buying what has fallen below target is, in essence, a disciplined implementation of "buy low, sell high" — without the risk of getting the timing wrong.

How Does DonkyCapital Help You Avoid Market Timing?

DonkyCapital is designed exactly for this: removing emotion from portfolio management. The system monitors your real allocation across all accounts and brokers in real time, comparing it with your target asset allocation. When drift exceeds your defined threshold, you receive an automatic alert — not an alarming notification, but a precise, actionable signal.

Asset class alert: DonkyCapital flags when equities exceed or fall below the target threshold

Alert-driven rebalancing: the system suggests the exact operations needed to return to target

The result is a radical transformation of the decision-making process: instead of asking "should I buy or sell now?" (market timing), you ask "has my portfolio drifted from target?" (systematic rebalancing). The first question requires predicting the future. The second requires only comparing two numbers. Fewer emotional decisions, more discipline, returns closer to your long-term potential.

FAQ on Market Timing and Rebalancing

Does market timing ever work, even for professionals?

In a consistent, replicable way over time, no. Buffett himself bet $1 million that no hedge fund would beat the S&P 500 over 10 years — and won.

What is the concrete difference between market timing and rebalancing?

Market timing is reactive and discretionary. Rebalancing is proactive and mechanical. The first requires being right twice. The second requires only discipline.

How often should I rebalance?

The most efficient approach is threshold-based: act when allocation drifts from target by a preset amount, typically 3–5%. This avoids over-trading in stable markets and ensures timely action when volatility creates significant drift.

What happens if I never rebalance?

Over time your portfolio drifts from target. If equities significantly outperform bonds, your equity share grows and you become much more exposed to risk than intended. In a bear market, this means losses far exceeding what you consciously accepted.

Do DonkyCapital rebalancing alerts replace a financial advisor?

Not for strategic planning. But for the operational side — monitoring drift and receiving timely signals — automatic alerts are often more precise and timely than any advisor who rarely monitors client portfolios in real time.

How do I resist the urge to sell everything during a major market crash?

The key is having a rule defined before the crash. If your plan says to rebalance when equities drop below a threshold, the crash becomes a buy signal — not a sell signal. DonkyCapital helps: instead of a vague feeling of panic, you receive a precise alert telling you exactly what to do according to your plan.

Does rebalancing have a tax cost from realized gains?

Yes, selling appreciated assets to rebalance can trigger taxable gains. A tax-efficient strategy prioritizes rebalancing through new capital contributions (buying underweight assets without selling) and using sales only when drift is significant or when there are losses to offset.

Start Rebalancing with Discipline

Set your target asset allocation on DonkyCapital and receive automatic alerts when it is time to rebalance — without emotion, without market timing.

Start for free