5 Fatal Portfolio Tracking Mistakes (That Cost Thousands of Euros)

Analyzing hundreds of portfolios imported into DonkyCapital, a recurring pattern emerges: most retail investors make the same systematic mistakes when tracking their investments. Mistakes that seem harmless individually but, accumulated over time, can cost thousands of euros in lost returns or wrong decisions based on incorrect data.

In this article we analyze the 5 most critical mistakes, with concrete numerical examples and practical solutions. For each one we'll also show how DonkyCapital prevents them automatically.

Mistakes index

Ignoring Transaction Fees

Transaction fees seem negligible individually — €2, €5, €10 per trade. But summed over time and compared to the capital they could have generated if reinvested, they become a significant cost that most investors never track.

Real impact — numerical example

- → Monthly ETF accumulation plan: 2 trades/month at €5 each = €120/year

- → On a €30,000 portfolio, €120/year = −0.40% of real return every year

- → Over 20 years, that €120/year invested at 7% = over €5,200 of lost capital

- → Adding the average TER of active ETFs (1.5% vs 0.2% for a passive ETF): the difference on €30,000 over 20 years exceeds €15,000

The problem isn't just the cost itself: without tracking them, you can't calculate the true net return and compare it correctly across different brokers or financial products.

The complete transaction log is the starting point for correctly tracking fees and costs.

How to avoid it

Record every transaction including the exact commission cost. DonkyCapital automatically aggregates costs into the net return calculation — so you can see the real cost of your portfolio, not just the gross gain.

Calculating Returns the Wrong Way

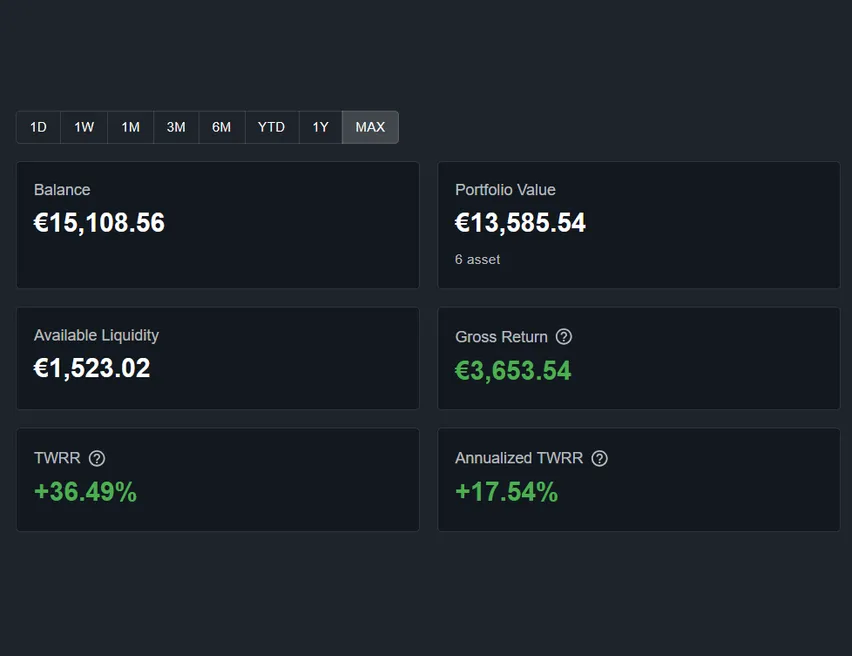

Your broker shows +83% performance. But are you really earning +83% per year? Almost certainly not. The number brokers show by default is the simple ROI: the difference between current value and total invested capital, without accounting for when you invested the individual amounts.

If you've made periodic contributions over the years, simple ROI can be very misleading compared to the true annualized return.

Practical example

- → Portfolio with TWRR +83% since the opening date

- → The same portfolio has an annualized TWRR of +33.5% per year

- → And a MWRR of +56% — the actual return on your specific capital

- → An investor who only reads "+83%" and thinks they're making +83% a year makes a huge mistake in their projections

DonkyCapital shows TWRR, annualized TWRR and gross return separately — so you'll never confuse the data.

How to avoid it

Always use TWRR to compare against benchmarks and MWRR/IRR to understand the actual return on your capital. Explore the differences in our guide to ROI, TWR and IRR.

Not Tracking Reinvested Dividends

Dividends are often considered an "extra" — a bonus that arrives every quarter and gets cashed in without being properly accounted for. It's one of the most costly mistakes in the long run.

Historically, dividends have contributed to over 40% of the total return of the S&P 500 over the last 50 years. Not tracking them means enormously underestimating real performance and losing visibility into the effect of compound interest over the long term.

Real impact — numerical example

- → You hold 100 Apple shares. Quarterly dividend: €0.25/share = €25 each quarter

- → €100/year reinvested in Apple for 15 years at 12% annual = €547 additional

- → On a €50,000 portfolio with 2% dividend yield: €1,000/year untracked

- → Over 20 years at 7% growth: over €40,000 of invisible return

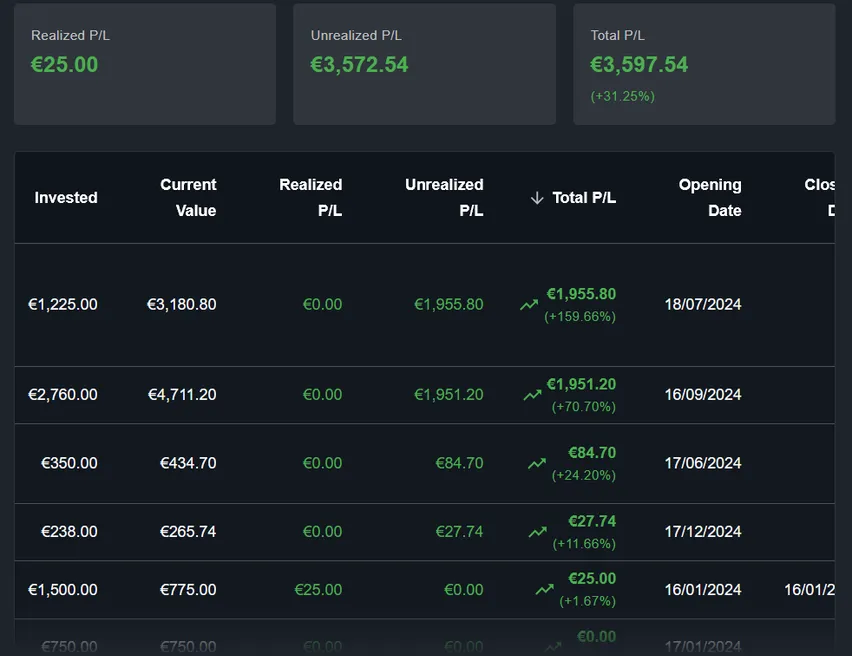

Note that in the transaction image above, the Apple dividend of January 18, 2024 (€25.00) is clearly recorded as a separate entry. Without this level of detail, your performance calculation is incomplete.

How to avoid it

Record every dividend payment as a separate transaction. If you reinvest them, also record the corresponding purchase. DonkyCapital includes dividends in the total return and realized P&L calculation automatically, without additional configuration.

Ignoring Currency Risk

Most European investors hold ETFs or stocks denominated in dollars — S&P 500, Nasdaq, American tech stocks. But many don't account for what happens when the EUR/USD exchange rate moves significantly.

Practical example — double currency effect

- → You buy an S&P 500 ETF when EUR/USD = 1.05

- → The ETF rises +20% in USD during the year

- → Meanwhile EUR/USD rises to 1.15 (EUR appreciates ~9.5%)

- → Your return in EUR: 1.20 / 1.095 − 1 = +9.6% (not +20%)

- → You "lost" over 10 percentage points of return due to the exchange rate

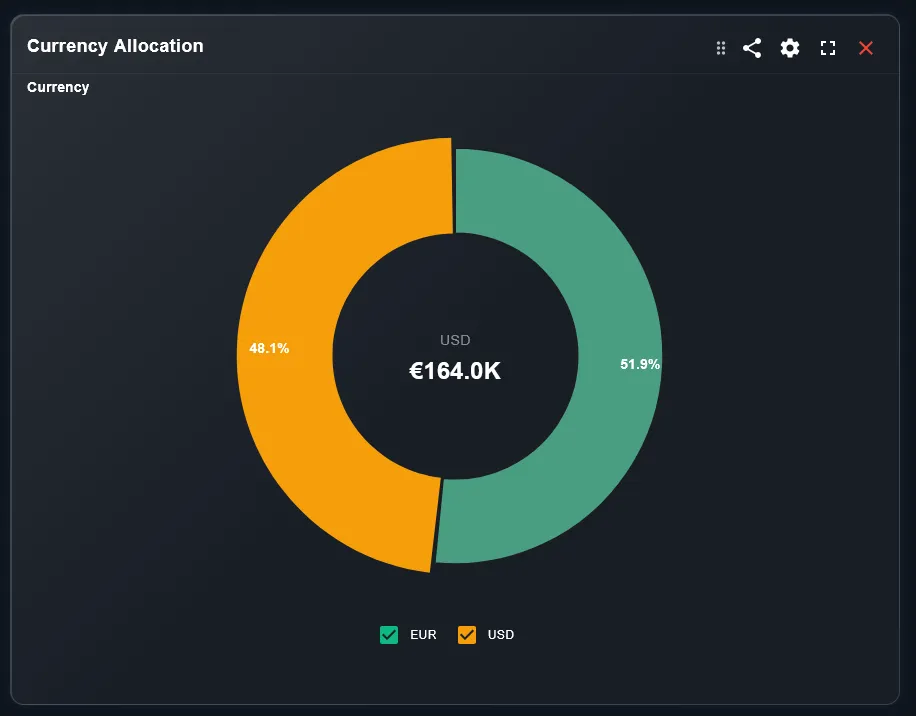

The phenomenon also works in reverse: a weak EUR amplifies gains on USD assets. The important thing is knowing how much currency exposure you have — and monitoring it over time.

Knowing the portfolio composition by asset class and geography helps assess currency exposure.

How to avoid it

Monitor your portfolio's currency allocation and always calculate returns in your reference currency (EUR). Consider whether a currency hedging quota is appropriate for your strategy — especially if you have >50% exposure in USD.

Not Accounting for Inflation

The portfolio grew +10% this year. Great result, right? It depends. If inflation over the same period was 4%, your real return — the one that truly matters in terms of purchasing power — was only +5.8%.

In the years 2021-2023, European inflation hit peaks of 10%. A portfolio that returned +7% in 2022 would have actually lost purchasing power in real terms. Ignoring this means systematically overestimating your wealth.

Real return formula

- → Nominal return: +10% | Inflation: +4%

- → Real return = (1.10 / 1.04) − 1 = +5.77%

- → Nominal return: +7% | Inflation: +10% (2022)

- → Real return = (1.07 / 1.10) − 1 = −2.7% (real loss!)

The performance chart shows nominal performance — remember to compare it with the inflation of the period to obtain the real return.

How to avoid it

Make it a habit to calculate real return by subtracting the period's inflation from the nominal return. For long-term evaluations, always use the European HICP (Harmonised Index of Consumer Prices) as a reference.

Learn how to track inflation in your portfolio with DonkyCapital →Bonus: Other Common Mistakes

Beyond the five main mistakes, here are other behaviors that compromise portfolio tracking quality:

- ⚠Tracking only one broker: With multiple accounts on different platforms, anyone who only aggregates the main one doesn't see the full picture. True performance is that of the consolidated portfolio. Learn more in the multi-broker tracking guide.

- ⚠Updating data infrequently: An Excel sheet updated once a month doesn't allow you to detect allocation drifts in real time.

- ⚠Confusing realized and unrealized P&L: Paper gains aren't gains until you sell. Treating them as equivalent leads to wrong decisions about when to liquidate a position.

- ⚠Not including cash in the portfolio: Available cash is capital that isn't earning. Not including it in the calculation distorts the real allocation and artificially reduces percentage performance.

- ⚠Ignoring capital gains taxes: In many countries, realized capital gains are taxed. Not considering this rate in the net return calculation leads to overestimating the actual result.

Full Checklist: Are You Making These Mistakes?

Use this checklist to verify the quality of your current tracking system:

- ✓I record every transaction with the exact commission included

- ✓I use TWRR (not simple ROI) to compare against benchmarks

- ✓I use MWRR/IRR to understand the actual return on my capital

- ✓I record every dividend received as a separate transaction

- ✓I reinvest dividends and record the corresponding purchase

- ✓I know my total currency exposure (% in USD, GBP, etc.)

- ✓I calculate real return by subtracting the period's inflation

- ✓I aggregate all brokers in a consolidated view

- ✓I keep realized and unrealized P&L separate

- ✓I include cash in the total allocation calculation

- ✓I consider the tax impact on capital gains in net return

If you're manually checking all these points on Excel, consider that DonkyCapital handles all of this automatically.

Tools That Prevent These Mistakes Automatically

The most effective solution for all five described mistakes is portfolio tracking software that handles these aspects automatically. Let's see how DonkyCapital addresses each of them.

✓ Fees

Every CSV import includes transaction fees in the net return calculation.

✓ Correct returns

TWRR, annualized TWRR and MWRR calculated automatically for every portfolio.

✓ Dividends

Dividends are automatically recognized from the import and included in realized P&L.

✓ Currency

Performance shown in the portfolio reference currency with automatic conversion.

DonkyCapital automatically separates realized and unrealized P&L for each position.

DonkyCapital supports import from Fineco, DeGiro, Scalable Capital, Directa and other European brokers. To learn how to import data from your specific broker, check our guides:

Frequently Asked Questions

Do these mistakes apply to ETF-only investors too?

Yes, all five apply to ETF investors. Purchase commissions, return calculation with periodic contributions (DCA), distributed dividends, currency exposure of physical replication ETFs, and the impact of inflation on real return are all relevant aspects for any investor, ETFs included.

Does the commission mistake apply to "zero commission" brokers too?

Yes. Zero commission brokers often recover costs through execution price spread, securities lending, or currency conversion. These implicit costs should also be estimated and included in the net return analysis.

How often should I check these parameters?

For fees and dividends: at every transaction. For returns and allocation: at least monthly. For currency effects and inflation: quarterly is sufficient for most retail investors.

Can these mistakes be corrected on an existing portfolio?

Yes, but it requires reconstructing the transaction history with all missing details. By importing your broker's historical CSV into DonkyCapital, the system automatically recalculates all metrics including dividends and fees present in the export.

Eliminate These Mistakes from Your Portfolio

DonkyCapital automatically handles fees, dividends, currency exchange, and correct return metrics — so you can focus on investment decisions, not calculations.

Access DonkyCapital for FreeFree Early Access · No credit card required