Goal-Based Portfolio Investing: How to Invest with Purpose

Most investors track their portfolio asking: "How much did I earn this month?" But that's the wrong question. The right question is: "Am I on track to reach my goal?" Goal-based investing flips the paradigm: instead of chasing abstract returns, you measure progress toward something concrete.

This guide explains what goal-based investing is, why it reduces market-driven stress, and how DonkyCapital lets you set financial goals — buying a house, early retirement, a new car — and track progress in real time with the Goal-Target widget.

What is Goal-Based Investing?

Goal-based investing is an investment philosophy that starts from the objective, not the return. Instead of asking "How do I maximise my annual return?", you ask "How much money do I need, and when?" Each portfolio becomes the vehicle to reach a specific, measurable goal.

The contrast with the traditional approach is stark: in classic portfolio tracking, the main metric is percentage performance. During downturns, this metric generates anxiety, impulses to sell, and irrational decisions. With goal-based investing, a -10% market drop is not a catastrophe if you're still ahead of your goal trajectory. The time horizon and concrete target act as behavioural shock absorbers, reducing panic selling and keeping focus on the long term.

University / Master's Fund

Accumulate capital to fund advanced studies without resorting to student loans.

Car Purchase

Save for the car you want, avoiding interest-bearing financing.

House Down Payment

Build the capital needed for a property down payment, reducing the mortgage required.

Sabbatical / Travel Fund

Fund a sabbatical year, an extended trip, or a career break without touching your main savings.

Early Retirement

Reach financial independence and stop working out of necessity before the traditional retirement age.

The Two Types of Goals in DonkyCapital

DonkyCapital supports two distinct modes for setting a financial goal on a portfolio. The choice depends on the nature of your target.

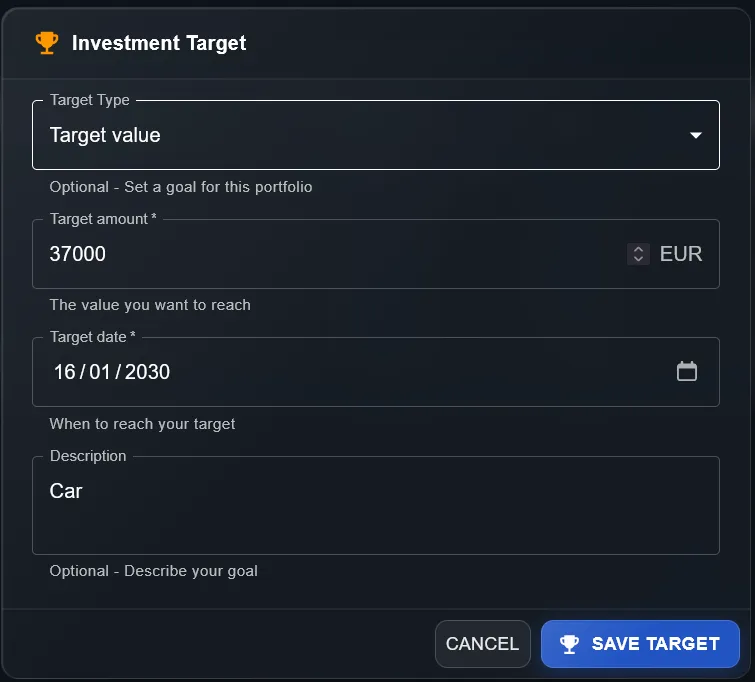

Target Value

You set a specific amount to reach by a date (e.g. €37,000 for a car by January 2030). DonkyCapital continuously compares your portfolio's current value with the target amount, calculating your financial progress percentage and comparing it against time elapsed. If you've reached 40% of the value but only 35% of the time has passed, you're ahead of schedule. Ideal for concrete goals with a defined amount.

Annual Growth Rate %

You set a target CAGR (e.g. 4% per year). DonkyCapital checks whether the portfolio is growing at the pace needed to maintain that rate until the target date. Useful for more abstract goals like "beat inflation", "grow by at least 6% per year", or "fund a master's with accelerated growth in one year". The system alerts you if the current pace is insufficient.

Target Value

Annual Growth Rate %

How to Set Up a Goal in DonkyCapital

Open the portfolio settings

Go to the portfolio you want to assign a goal to and access its settings. Each portfolio can have an independent goal — if you have multiple goals, create a separate portfolio for each one.

Select "Investment Target" and choose the type

In the Investment Target section, choose the goal type: "Target Value" if you have a specific amount to reach, or "Annual Growth Rate %" if you want to monitor a compound annual growth rate.

Fill in the parameters and save

Enter the amount or rate, the target date, and an optional description (e.g. "Car", "Master's", "House"). This description appears in the widget to keep you reminded of the "why" behind your investing.

The Goal-Target widget updates automatically

After saving, the Goal-Target widget on your dashboard starts tracking progress in real time. You can add it to your dashboard from the widgets section if it's not already visible.

How to Read the Goal-Target Widget

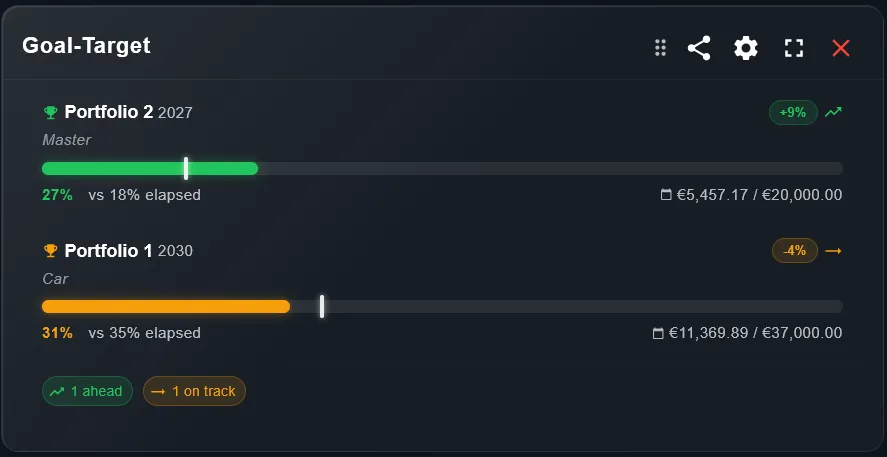

Progress bar colour

Green = you're ahead of the linear trajectory. Orange = you're slightly behind but the gap is recoverable. Red = you're significantly behind and corrective action is likely needed.

Financial % vs Time elapsed %

The crucial comparison: if your financial progress (% of target reached) exceeds your temporal progress (% of time elapsed from start to target date), you're ahead. Example: 40% of value reached with 35% of time elapsed = you're 5% ahead.

Badge (+9% / -4%)

The badge shows how far ahead or behind you are relative to the linear trajectory toward the goal. A +9% means your financial progress exceeds the temporal one by 9%. A -4% signals a slight delay to monitor.

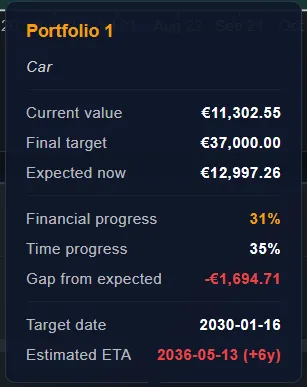

Gap from expected (in detail view)

In the detail view, you see the euro gap between your portfolio's current value and the value you should have "now" according to the linear trajectory. Example: current value €11,302, expected value €12,997 → gap of -€1,694.

Estimated ETA

If you continue at the current pace, when will you reach your goal? If the ETA shows "+6 years" beyond the target date, it's a clear warning signal: without increasing contributions or returns, you won't make it in time.

Advanced Reading: Understanding the Detail View

Let's analyse a real example using the detail view data. Portfolio "Car": target €37,000 by January 2030. Current value: €11,302. Expected value now (linear interpolation from start date to January 2030): €12,997. Gap: -€1,694 below the expected value.

Financial progress: 31% of target reached. Time progress: 35% of time elapsed. Result: you're slightly behind schedule (-4%). Projected ETA at the current pace: 2036 — six years behind the goal.

What does this mean in practice? At the current pace, you won't reach €37,000 in 2030 but in 2036. This isn't necessarily a catastrophe, but it's an action signal: you can increase monthly contributions, revise the target date, or review your portfolio allocation toward assets with a higher expected return (accepting greater risk).

Strategies When You're Behind

Increase monthly contributions

The most direct and predictable lever: add capital every month. Even small increases in regular contributions have a significant impact thanks to compound interest over the long term. Calculate how much you need to add each month to close the gap using DonkyCapital.

Adjust the target date

Sometimes the most rational response is to re-evaluate the time horizon. If the car can wait until 2032 instead of 2030, the gap disappears without doing anything extraordinary. Modify the target date in the portfolio settings and immediately see the impact on the widget.

Review your asset allocation

A portfolio that is too conservative (e.g. all cash or short-term bonds) may not generate the return needed to reach the goal on time. Consider shifting a portion of capital toward global equity ETFs, accepting more volatility in exchange for a higher expected return over the long term.

FAQ

Can I have multiple goals at the same time?

Yes. In DonkyCapital, each portfolio can have an independent goal. To have multiple goals in parallel, create a separate portfolio for each one: one for the car, one for the house, one for the master's degree. The consolidated dashboard shows all portfolios together, but each goal is tracked independently.

What happens if I pass the target date without reaching the goal?

DonkyCapital shows an updated ETA projection indicating how many years or months behind you are relative to the original target. You can modify the target date in the settings to update the trajectory, or use the warning signal to increase contributions or review your allocation.

Is the annual rate goal the same as a benchmark?

No, they are different concepts. The Annual Growth Rate % goal measures the absolute growth of your portfolio: you want it to grow by 4% per year, regardless of how the market behaves. A benchmark, on the other hand, measures relative performance: it compares your portfolio against a reference index (e.g. MSCI World). You could beat the benchmark but not meet your rate goal — or vice versa.

How do I choose between "Target Value" and "Annual Growth Rate"?

Use "Target Value" when you have a specific amount to reach by a date: €37,000 for a car, €80,000 for a house down payment. Use "Annual Growth Rate %" when your goal is more abstract: beating inflation, growing at 5% per year, or funding a master's in one year. The former is more concrete and intuitive; the latter suits pure performance goals.

Can I change my goal after setting it?

Yes, you can update the target value, target date, or annual rate at any time from the portfolio settings. The widget recalculates the trajectory automatically. It's perfectly normal to recalibrate goals over time — especially after life events like a job change or an unexpected expense.

What does "Gap from expected" mean in the detail view?

"Gap from expected" is the euro difference between the value you should have accumulated today (according to the linear trajectory toward the target) and your actual current value. A negative gap (e.g. -€1,694) means you're behind the ideal trajectory. It doesn't necessarily mean you'll miss the goal, but that your current pace needs to accelerate.

Does the estimated ETA account for future contributions?

The estimated ETA is calculated by projecting your portfolio's current growth rate without assuming any new contributions. It's therefore a conservative estimate: if you keep investing monthly, the actual date will likely be closer to the target. Use it as a warning signal, not an absolute forecast.

Can I use goal-based investing with a regular investment plan (DCA)?

Absolutely — it's the ideal combination. Set a "Target Value" goal with your DCA end date, and use the Goal-Target widget to verify each month whether you're accumulating enough. If the gap grows, you can increase your monthly contribution or extend the duration.

Start Investing with Purpose

Create your free account and set up your first financial goal in less than 5 minutes. No credit card required.

Create Free Account